Building Societies have been part of our communities for 250 years.

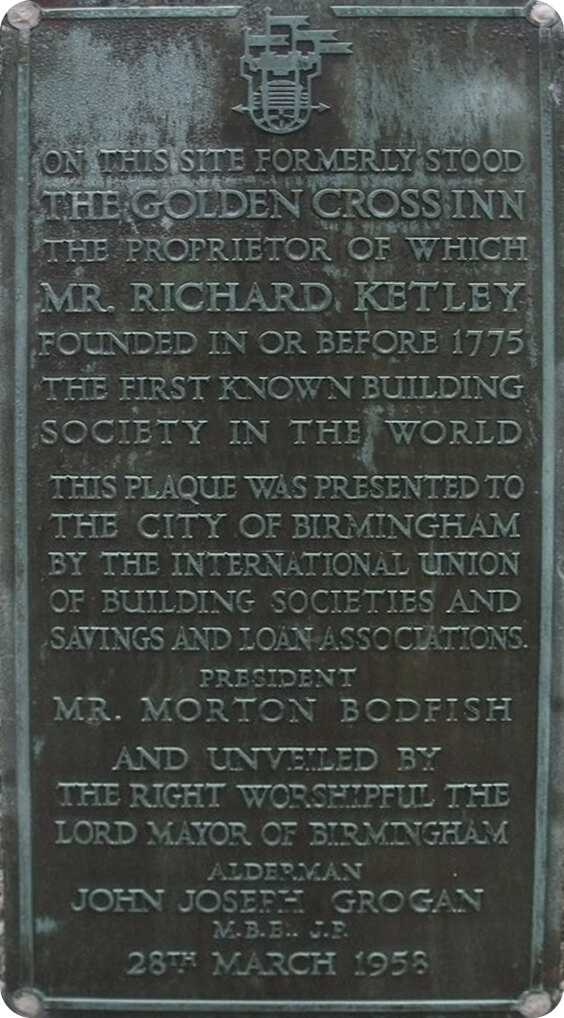

In 1775, Richard Ketley, the landlord of the Golden Cross Inn in Birmingham, got his regulars to pool their savings each week. When there was enough money in the pot, they used it to buy land and build a home. They drew lots to determine which of them would get the home. They all carried on saving and building houses until each member owned their own home. Ketley’s Building Society was the first ever Building Society.

There are 42 Building Societies in the UK today, with over 25 million members, more than 1,300 branches on our high streets and they employ around 52,500 people.

Credit Unions are member-cooperatives, providing savings and loans to these members who all share a common bond. This typically means they are either based in their local community or their members work in the same sector, e.g. the police. Credit Unions promote regular saving, offer personal loans and some also provide mortgages. Their members’ needs are at the heart of their business. The first Credit Unions in the UK started in the 1960s, often founded by recent immigrants with experience of Credit Unions in both the West Indies and Ireland.

Building Societies and Credit Unions are still owned and run for the benefit of their members, the customers, and all profits are reinvested back into the business, which is reflected in their rates, products and services.

Genuinely committed to supporting communities

From charity fundraising to community projects, read how Building Societies & Credit Unions work with their communities.

Helping Dementia UK’s Admiral Nurses

Nationwide Building Society Fairer Futures will fund an additional 30 experienced, compassionate dementia specialist nurses.

New branch in Solihull

Leeds Building Society has opened a new branch in Solihull, demonstrating their commitment to the high street and face to face financial services.

Helping to fight food poverty

Cumberland Building Society made its biggest-ever charity donation, committing £500,000 over two years to help combat food poverty.

Partnering with over 90 organisations offering payroll savings

Capital Credit Union partners with organisations to offer Payroll Savings, which makes it easy for staff to save for emergencies or special occasions.

Employability programme helps hundreds

A partnership between Yorkshire Building Society and charity FareShare is celebrating helping over 450 people improve their employability prospects.

Partnering with a local hospice

Loughborough Building Society has partnered with Rainbows Hospice for Young showing a commitment to supporting their vital work.

Volunteering with Mission Christmas

Vernon Building Society employees volunteered to pack presents with Cash for Kids for their Mission Christmas appeal.

Investing in face-to-face financial services

Newcastle Building Society continues to invest in their branch network with the reopening of their Hartlepool branch and relocation of their Middlesbrough branch.

Sponsoring Edinburgh Rugby women's team

Scottish Building Society is expanding their partnership with Edinburgh Rugby to include front-of-shirt sponsor of the women’s team.

All together, for each other

The Building Societies Association

The Building Societies Association (BSA) was established in 1869. It is the voice for all 42 UK building societies, including both mutual banks, and 7 of the largest Credit Unions.